📈 Wyckoff SMI “Week In Review” April 5th, 2026.

📋 Market ScoreCard

- SPY — Distribution → Markdown (SOW / FTI active)

- QQQ — Distribution → Early Markdown (weaker structure than SPY)

- TLT — Weak Rally within Larger Downtrend (supply dominant)

- GDX — Distribution resolving lower (UTAD → AR → breakdown)

- XLE — Strong Markup (leading sector, controlled trend)

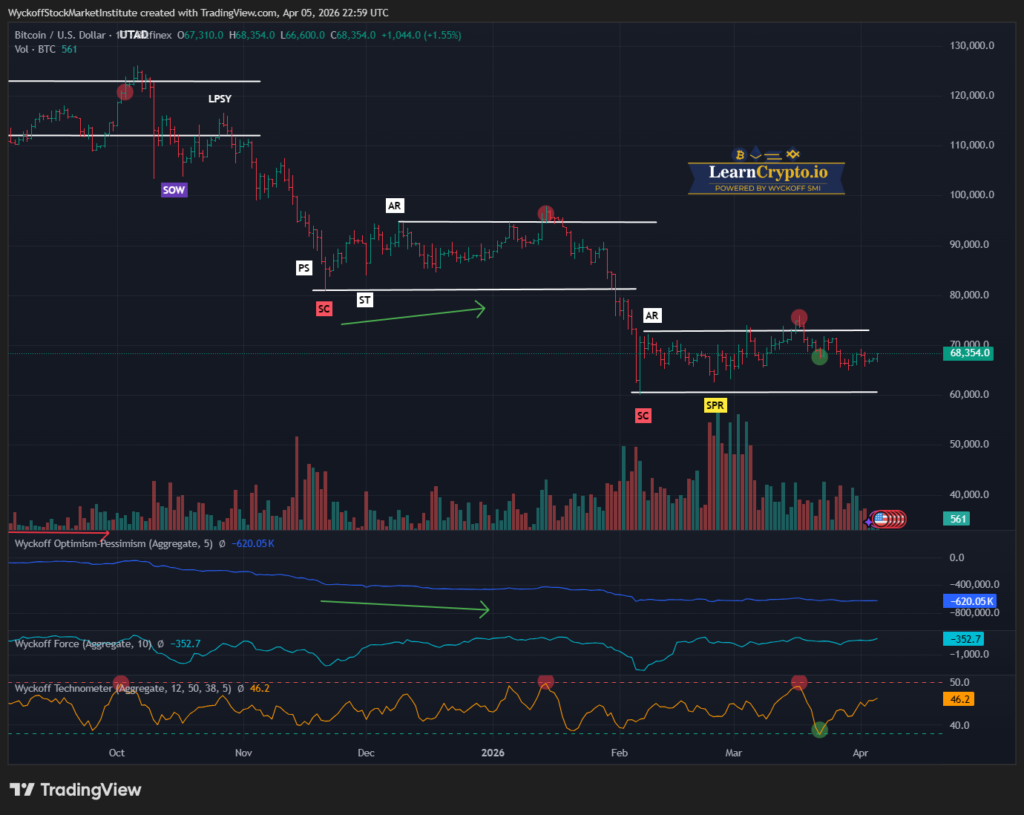

- BTC — Range-bound / Re-Accumulation Attempt

- ETH — Early Accumulation (SC → AR → ST → JAC emerging)

🌍 Macro Market Backdrop

This week’s price action continues to reflect tightening financial conditions, with the key driver remaining rising inflation expectations tied to geopolitical instability and higher oil prices.

The sharp selloff in bonds (TLT) signals persistent upward pressure on yields, which continues to weigh on equity valuations—particularly growth.

From a Wyckoff perspective, the macro backdrop remains hostile to broad risk-on behavior, favoring selective leadership (energy) while the broader market transitions through distribution into markdown.

🧭 Market Overview (SPY / QQQ)

SPY continues to confirm a distributional structure, with prior UTAD/TOU activity now resolving into SOW → FTI → MKDN behavior.

Rallies are shallow, failing near prior support (now resistance), and downside continuation is becoming more orderly and controlled, characteristic of institutional markdown rather than panic liquidation.

Effort vs. result confirms weakness: selling pressure is persistent, while demand is unable to produce meaningful upside follow-through.

QQQ remains structurally weaker than SPY and is further along in the markdown sequence.

The recent breakdown below support confirms a clean FTI, followed by continued lower highs and expanding downside range.

Tech continues to act as the pressure point of the market, reflecting sensitivity to higher rates and tighter liquidity conditions.

🏦 Interest Rates & Defensive Assets (TLT)

TLT experienced a sharp and aggressive selloff this week, reinforcing the message that rates are not stabilizing — they are reaccelerating higher.

From a Wyckoff standpoint, this is classic supply dominance following failed rally attempts, leading into renewed markdown.

This is critical:

- Rising yields = tightening conditions

- Tightening conditions = pressure on equities

This dynamic is now clearly feeding into broader market weakness and is a primary driver behind the current equity markdown phase.

⛏️ Gold / Hard Assets (GDX)

GDX continues to unwind from a prior distribution structure, where a BC → led into weakness.

Despite the inflation narrative, gold miners are not acting as a leadership group, suggesting that:

- This is not yet a full “flight to safety” environment

- Capital is rotating elsewhere (not into gold equities)

The recent bounce appears reactive rather than structural, with supply still controlling the tape.

⚡ Energy Sector (XLE)

XLE remains the clear institutional leader.

The structure shows a textbook Wyckoff markup sequence:

- Accumulation base

- JAC (Jump Across Creek)

- BU / LPS continuation behavior

- Sustained trend channel higher

Importantly, pullbacks remain controlled and low-effort, signaling continued institutional sponsorship.

Energy is benefiting directly from the macro backdrop, particularly elevated oil prices tied to geopolitical tensions, making it the dominant theme in the current market environment.

₿ Crypto Market Overview (BTC / ETH)

Bitcoin remains in a broad trading range, attempting to stabilize after prior markdown.

The structure suggests early re-accumulation potential, but lacks a decisive SOS / JAC confirmation.

Momentum is improving slightly, but BTC remains in a neutral-to-developing phase, requiring confirmation before turning constructive.

Ethereum is showing a more constructive structure relative to BTC.

The chart reflects:

- SC → AR → ST sequence completed

- Emergence of a JAC (Jump Across Creek)

- Holding above support with improving structure

This suggests early Phase D behavior, though confirmation is still required. ETH is currently one of the more technically constructive crypto setups.

🔄 Rotational & Thematic Notes

- Energy (XLE) — Clear leadership; strongest institutional flow

- Equities (SPY / QQQ) — Broad distribution resolving into markdown

- Rates (TLT) — Primary macro pressure driver

- Gold (GDX) — Weak relative performance despite inflation backdrop

- Crypto — Early stabilization, ETH showing relative strength

The key theme remains:

👉 Selective leadership in a weakening macro environment

🧠 Tactical Outlook

The market is transitioning from distribution into early-to-mid markdown, with rallies increasingly functioning as short-term countertrend moves rather than structural reversals.

Until:

- Rates stabilize

- Demand re-enters equities with conviction

…the path of least resistance remains lower for broad indices.

Meanwhile, sector rotation remains critical, with energy continuing to provide the clearest opportunities.

👉 What We’re Watching Now

- Continued SOW → FTI follow-through in SPY / QQQ

- Whether TLT selling accelerates further (rates breakout risk)

- Any signs of demand returning in equities (SOS attempts)

- Sustainability of XLE leadership trend

- Confirmation of ETH Phase D (hold above JAC)

🎯 ProTraders CTA

If you’re serious about understanding what the market is actually doing — not what the headlines say — this is where you need to be.

👉 Join WyckoffSMI ProTraders and trade alongside a professional Wyckoff framework:

WyckoffSMI.com

⚠️ Disclaimer

The WyckoffSMI Week In Review is provided for educational and informational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any security. All commentary reflects a Wyckoff-structure interpretation at the time of publication and may change as market conditions evolve.

Investing involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. WyckoffSMI and affiliated entities may hold positions in securities discussed. Readers are solely responsible for their own investment decisions and should consult a qualified financial professional before acting.

Responses