📈 Wyckoff SMI “Week In Review” March 28th, 2026.

📋 Market ScoreCard

- SPY → Distribution → Markdown (SOW → FTI → MKDN)

- QQQ → Distribution → Markdown Acceleration

- TLT → Weak / Failing Rally → Supply Dominant

- GDX → Distribution Emerging (Post-Climax Behavior)

- XLE → Markup → Extended (Profit-Taking Zone)

- BTC → Distribution → Early Re-Accum Attempt Failing

- ETH → Distribution → Weak Re-Accumulation Range

🌍 Macro Market Backdrop

Markets were rattled this week as geopolitical tensions and rising energy prices fueled renewed inflation concerns. The sharp selloff in bonds reflects a market repricing higher rates, which is pressuring equities broadly.

This is a classic Wyckoff backdrop where liquidity is tightening, and institutions are transitioning from distribution into markdown across risk assets. Rising oil prices are acting as a secondary tightening mechanism, reinforcing inflation expectations and limiting the Fed’s flexibility.

The result:

- Risk assets weakening

- Rates rising

- Volatility expanding

This is not an environment supportive of aggressive long exposure.

🧭 Market Overview (SPY / QQQ)

Both SPY and QQQ continue to confirm a clear distribution → markdown transition.

SPY has now broken down from its trading range with a clean SOW → FTI sequence, followed by continued MKDN behavior. Rallies are shallow and failing quickly, which is a key hallmark of institutional supply remaining in control.

QQQ is even weaker structurally, showing:

- Multiple UTAD / TOU failures

- Inability to reclaim prior support

- Expanding downside spread

The key takeaway is simple:

Demand is absent, and supply is dominant.

This is not consolidation — this is active markdown.

🏦 Interest Rates & Defensive Assets (TLT)

TLT weakened again this week, reinforcing the idea that the bond market is not yet providing a defensive tailwind to equities. Structurally, the ETF appears to have failed after a rally attempt, with prior UTAD behavior folloTLT experienced a sharp selloff this week, driven by inflation fears tied directly to rising energy prices and geopolitical instability.

From a Wyckoff perspective, TLT is:

- Failing to sustain rallies

- Showing repeated supply signatures

- Breaking down from attempted support zones

This is a bearish signal for bonds and a headwind for equities.

Rising yields are tightening financial conditions, and the equity market is responding accordingly.

This dynamic is critical — stocks are not falling in isolation; they are reacting to a bond market repricing risk.

⛏️ Gold / Hard Assets (GDX)

GDX is beginning to show early distribution characteristics following a strong markup phase.

Recent price action reflects:

- Climactic behavior (BC-type action)

- UTAD attempts near highs

- Failure to hold strength

While gold has benefited from macro uncertainty, the miners are now showing supply entering the market.

This suggests:

- Smart money may be locking in profits

- Upside momentum is stalling

This is not yet confirmed markdown, but it is no longer clean markup.

⚡ Energy Sector (XLE)

XLE remains the clear leader, continuing its strong markup trend.

However, structurally:

- Price is extended within its channel

- Momentum is elevated

- Public participation is increasing

This is exactly where institutions begin to scale out of positions.

👉 As noted: We are actively watching to take large profits on our long positions.

This is not a short — but it is late-stage markup, where risk/reward begins to deteriorate.

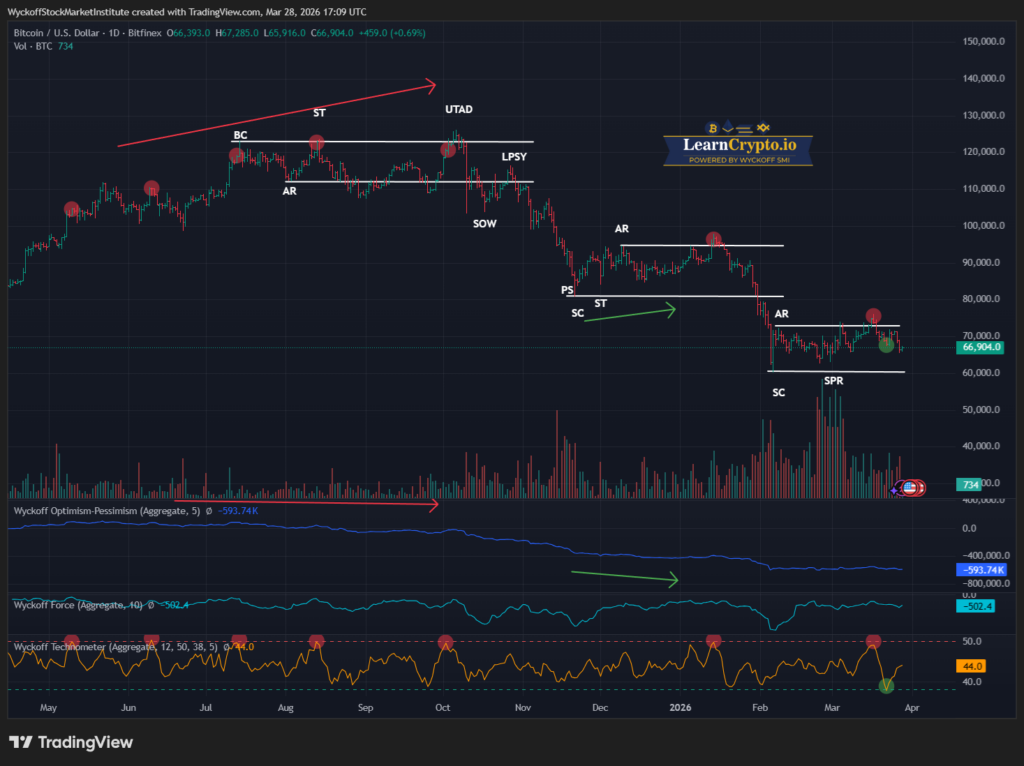

₿ Crypto Market Overview (BTC / ETH)

Crypto markets continue to struggle under the weight of distribution.

Bitcoin (BTC):

- Completed a clear distribution structure (BC → UTAD → SOW)

- Attempted re-accumulation is weak and failing to gain traction

- Lower highs continue to define the structure

👉 We were stopped out at breakeven on last week’s trade — a disciplined outcome in a weak environment.

Ethereum (ETH):

- Similar structure to BTC, but weaker overall

- Trading in a shallow range with no demand expansion

- Failed attempts to reclaim resistance

👉 Also stopped out at breakeven, confirming lack of follow-through.

The key takeaway:

Crypto is not yet ready — demand has not returned.

🔄 Rotational & Thematic Notes

- Capital is rotating out of growth (QQQ)

- Defensive positioning is increasing, but not cleanly trending

- Energy remains the only strong sector — but now late-stage

- Bonds are breaking down, removing a key support pillar for equities

- Crypto remains risk-off correlated, not acting as a hedge

- This is a broad risk-off environment, not an isolated sector move.

🧠 Tactical Outlook

The weight of evidence remains firmly bearish.

We are seeing:

- Confirmed markdown in equities

- Rising yields pressuring valuations

- Weak participation across risk assets

- Late-stage strength in energy

This is a capital preservation environment, not an aggressive opportunity environment.

👉 What We’re Watching Now

- Continuation of SPY / QQQ markdown

- Any oversold rally attempts (likely to fail initially)

- TLT stabilization or further breakdown (critical macro signal)

- XLE exhaustion signals (profit-taking window)

- Crypto: waiting for true accumulation signals (not present yet)

🎯 ProTraders CTA

Markets are no longer rewarding passive participation — they are rewarding precision, timing, and structure.

Right now, we are seeing:

- Distribution and breakdown behavior in the major indexes

- Persistent leadership in select sectors like energy

- Emerging opportunity developing beneath the surface in crypto

This is exactly the type of environment where the Wyckoff Method separates professionals from the crowd.

Inside WyckoffSMI ProTraders, we are:

- Identifying institutional accumulation and distribution in real-time

- Tracking sector rotation before it becomes obvious

- Providing high-probability campaign setups using our proprietary tools

- Using the Wyckoff Technometer to time market turns with precision

If you’re serious about understanding what the market is actually doing — not what the headlines say — this is where you need to be.

👉 Join WyckoffSMI ProTraders and trade alongside a professional Wyckoff framework:

WyckoffSMI.com

⚠️ Disclaimer

The WyckoffSMI Week In Review is provided for educational and informational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any security. All commentary reflects a Wyckoff-structure interpretation at the time of publication and may change as market conditions evolve.

Investing involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. WyckoffSMI and affiliated entities may hold positions in securities discussed. Readers are solely responsible for their own investment decisions and should consult a qualified financial professional before acting.

Responses