📈 Wyckoff SMI “Week In Review” May 10th, 2026.

📋 Market ScoreCard

| Symbol | Condition | WyckoffSMI View |

|---|---|---|

| SPY | Bullish | Breakout trend intact, extended short-term |

| QQQ | Bullish | Technology leadership accelerating |

| TLT | Bearish Bias | Weak range structure, lower favored |

| GDX | Neutral | Stabilizing after testing prior lows |

| XLE | Corrective | Pullback followed expected overbought signal |

| BTC | Bullish | Slow steady markup continuing |

| ETH | Neutral Bullish | Consolidating inside constructive structure |

Wyckoff Market Health Dashboard

- Market Health Score: 56

- Health: NEUTRAL/IMPROVING

- Execution: MODERATE

- Trend: TRENDING UP

- Confirmation: WEAK

- Condition: STABILIZING/IMPROVING

- Cluster: WARNING

- Regime: TRANSITION/SELECTIVE BULLISH

Leadership

- Semiconductors (SMH)

- Technology (XLK)

- Speculative Growth (ARKK)

Weakness

- Financials (XLF)

- Health Care (XLV)

- Software (IGV)

Tactical Positioning

Overweight: XLK, SMH, ARKK

Underweight: XLF, XLV, IBB

🌍 Macro Market Backdrop

Markets continue operating inside a constructive bullish regime as institutional capital remains concentrated in technology, semiconductors, and speculative growth leadership.

The broad market remains strong structurally, but momentum is increasingly stretched after several weeks of persistent upside continuation. While price action remains bullish overall, the market continues to look vulnerable to a healthy short-term pullback or consolidation phase.

Participation beneath the surface remains mixed, reinforcing the importance of staying aligned with dominant leadership rather than broad diversification into weaker sectors.

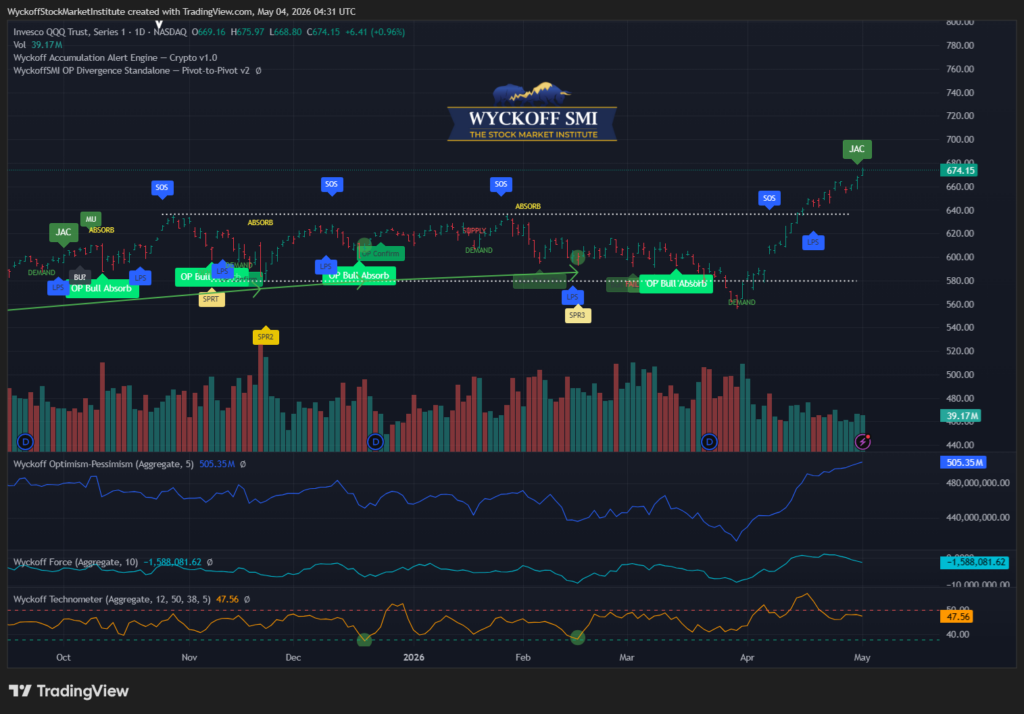

🧭 Market Overview (SPY / QQQ)

SPY continues trending higher after confirming another successful breakout continuation sequence. Price action remains firmly constructive as institutions continue supporting the advance.

However, after the recent acceleration higher, conditions are becoming increasingly extended short-term. While there are no major structural breakdown signals currently present, the market would likely benefit from a controlled pause or pullback before attempting another major leg higher.

Momentum remains positive, but tactical risk/reward is becoming less favorable for aggressive new long exposure at current levels.

QQQ remains the dominant leadership index as technology and semiconductor strength continue driving market performance. The recent breakout continuation confirms that institutional sponsorship remains concentrated inside growth leadership.

Relative strength continues improving versus the broader market, though Technometer conditions are approaching elevated levels again. The trend remains higher overall, but conditions are becoming crowded and increasingly dependent on continued technology participation.

For now, leadership remains intact.

🏦 Interest Rates & Defensive Assets (TLT)

TLT remains trapped inside a weak sideways structure while continuing to fail at key resistance levels. Technometer readings remain neutral, but the broader distribution framework continues favoring lower prices over time.

We continue maintaining a bearish stance toward long-duration bonds and expect eventual downside resolution from the current consolidation range.

The inability of bonds to attract sustained upside participation despite periods of market uncertainty remains an important intermarket signal.

⛏️ Gold / Hard Assets (GDX)

Precious metals behaved largely as expected this week, successfully testing previous lows while Technometer readings remained neutral. The sector continues attempting to stabilize following its prior correction phase.

Although upside momentum remains limited for now, the successful retest of prior support is constructive short-term and suggests selling pressure may be gradually moderating.

GDX remains an important rotational group to monitor if institutional leadership begins broadening beyond technology.

⚡ Energy Sector (XLE)

Last week’s overbought Technometer condition correctly preceded a period of selling pressure and consolidation inside XLE. The sector remains inside a broader constructive structure, but upside momentum clearly slowed following the prior rebound.

Price action now appears to be transitioning into a more neutral corrective phase after the strong tactical rally from oversold conditions.

For now, energy remains a secondary leadership group behind semiconductors and technology.

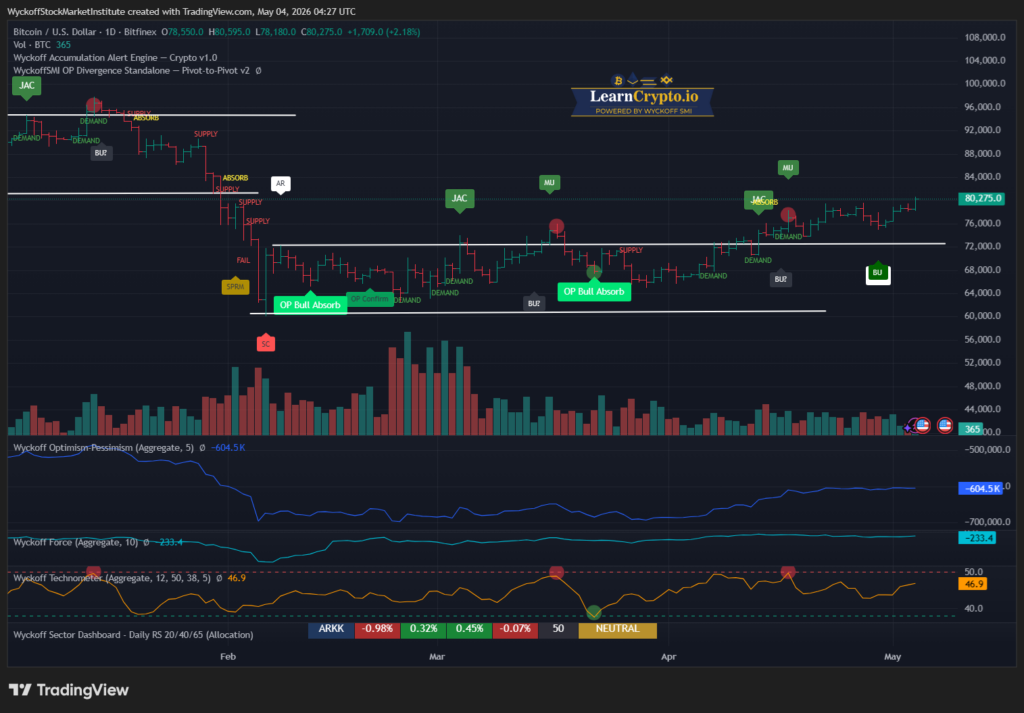

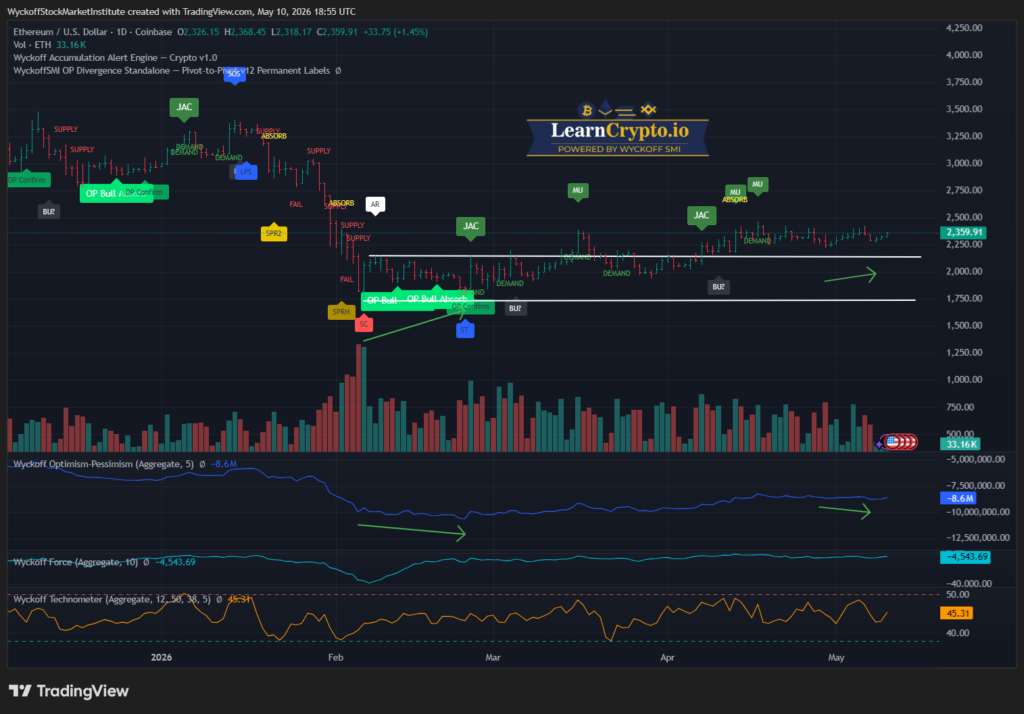

₿ Crypto Market Overview (BTC / ETH)

Bitcoin continues advancing steadily higher while maintaining its bullish recovery structure. Price action remains orderly and constructive as institutions continue supporting the gradual markup phase.

Technometer conditions are elevated but not yet fully overbought, suggesting there may still be room for additional upside continuation before momentum becomes stretched.

Bitcoin remains one of the stronger risk-on leadership areas currently developing across markets.

Ethereum continues consolidating within a constructive neutral-bullish structure. Unlike prior weeks, Technometer readings have cooled back toward neutral territory, reducing immediate overbought concerns.

ETH continues lagging Bitcoin slightly on a relative basis but remains structurally healthy overall as long as recent support levels continue holding.

The broader crypto environment remains constructive for now.

🔄 Rotational & Thematic Notes

Leadership Remains Concentrated In:

- Semiconductors (SMH)

- Technology (XLK)

- Speculative Growth (ARKK)

Weakness Persists In:

- Financials (XLF)

- Software (IGV)

- Defensive sectors

Key Rotational Themes:

- Technology continues dominating institutional flows

- Bitcoin remains a strong speculative risk-on proxy

- Bonds continue failing to stabilize structurally

- Precious metals attempting stabilization

- Energy momentum cooling after prior rebound

🧠 Tactical Outlook

The market remains inside a bullish regime, but conditions increasingly favor tactical patience over aggressive chasing.

Our primary focus remains:

- Staying aligned with dominant leadership

- Managing risk as extension increases

- Monitoring for pullback opportunities

- Avoiding structurally weak lagging sectors

Technology and semiconductors continue carrying the market, but increasingly stretched conditions suggest traders should become more selective with positioning near-term.

The trend remains higher — but extension risk is rising.

👉 What We’re Watching Now

- Can SPY / QQQ continue higher without broader participation?

- Does TLT finally break lower from its prolonged range?

- Will GDX continue stabilizing after its support retest?

- Does XLE complete its corrective phase?

- Can Bitcoin continue advancing without reaching overbought extremes?

- Will Ethereum begin improving relative strength versus BTC?

🎯 ProTraders CTA

Inside WyckoffSMI ProTraders, members receive:

- Institutional Wyckoff market analysis

- Sector rotation dashboards

- Relative strength leadership tracking

- Wyckoff Alert Engine signals

- Tactical positioning updates

- Crypto and equity market intelligence reports

Join WyckoffSMI ProTraders to track institutional positioning in real time.

👉 Join WyckoffSMI ProTraders and trade alongside a professional Wyckoff framework:

WyckoffSMI.com

⚠️ Disclaimer

The WyckoffSMI Week In Review is provided for educational and informational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any security. All commentary reflects a Wyckoff-structure interpretation at the time of publication and may change as market conditions evolve.

Investing involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. WyckoffSMI and affiliated entities may hold positions in securities discussed. Readers are solely responsible for their own investment decisions and should consult a qualified financial professional before acting.

Responses