📈 Wyckoff SMI “Week In Review” July 5th, 2026.

📋 Market ScoreCard

| Symbol | Trend | WyckoffSMI View |

|---|---|---|

| SPY | Range / Corrective | Five-week consolidation continues as correction unfolds beneath the surface. |

| QQQ | Range / Mixed | Technology remains resilient but momentum continues to fade. |

| TLT | Bearish | Violent reversal reinforces our bearish outlook; we continue looking for lower prices. |

| GDX | Bearish | Relief rally continues, but larger downtrend remains intact. |

| XLE | Bullish LT | Sideways consolidation within a longer-term bullish structure. |

| BTC | Corrective | Pullback followed our overbought signal; still waiting for a low-risk long entry. |

| ETH | Corrective | Improving modestly but confirmation remains incomplete. |

🧮 Wyckoff Market Health Dashboard

Market Health Score: 54

This week’s dashboard improved modestly and reflects a market that continues stabilizing beneath the surface.

- Health: Neutral / Improving

- Execution: High

- Trend: Range / Mixed

- Confirmation: Strong

- Condition: Stabilizing / Improving

- Cluster: Breakout

- Regime: Transition / Selective Bullish

Although the Market Health Score has improved, the mixed trend reading suggests this remains a stock-picker’s market rather than a broad-based bull market. Leadership has narrowed toward Semiconductors and Biotechnology while many sectors continue consolidating. Overall, market internals have improved from prior weeks, but we still prefer selective exposure over aggressive index investing.

🌍 Macro Market Backdrop

Markets continue digesting months of gains through time rather than price. While major indexes remain resilient, sector leadership continues rotating beneath the surface as institutional money selectively reallocates capital. The combination of a stronger U.S. Dollar outlook and expectations for higher interest rates continues shaping our macro view across equities, commodities, and digital assets.

🧭 Market Overview (SPY / QQQ)

SPY has spent more than five weeks trading in a broad sideways range. While price has held together remarkably well, we continue viewing this action as a correction occurring through time rather than a fresh markup phase. Until the index can break decisively from this range with improving internals, we remain cautiously optimistic but selective.

QQQ continues outperforming many other sectors, although momentum has cooled considerably. Technology remains one of the strongest leadership groups, but participation underneath the surface remains inconsistent. We continue watching for broader market confirmation before becoming more aggressive.

🏦 Interest Rates & Defensive Assets (TLT)

Following the recent rally, TLT experienced a sharp reversal that reinforces our longer-term bearish thesis. We continue holding our short position and believe the recent bounce was simply another rally within a larger topping process. Unless bond prices can reclaim recent highs, we continue expecting lower prices ahead.

⛏️ Gold / Hard Assets (GDX)

Gold miners finished slightly higher during the week, but the larger trend remains negative. Our expectation of a stronger Dollar and higher interest rates continues to weigh on the precious metals complex. While an intermediate-term low may eventually develop, we still believe additional downside remains possible before that process completes.

⚡ Energy Sector (XLE)

XLE spent another week moving sideways as crude oil remained under pressure. Despite the lack of upside momentum recently, our longer-term outlook remains constructive. We continue viewing this as a consolidation phase within a larger bullish trend and remain long.

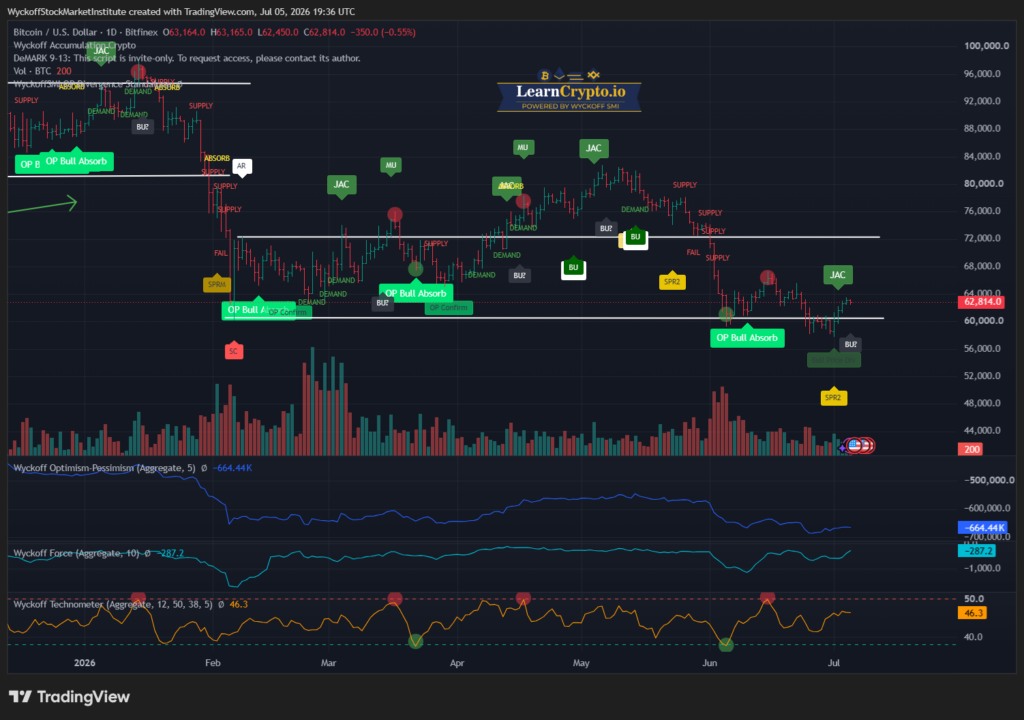

₿ Crypto Market Overview (BTC / ETH)

Bitcoin continued lower following the overbought Technometer signal we highlighted several weeks ago, behaving largely as expected. The market did stage a rally during the week, but our indicators never aligned to provide the type of low-risk institutional entry we prefer. We remain patient and continue monitoring for an oversold condition that could provide a higher-probability buying opportunity.

Ethereum remains weaker than prior bull cycles but has shown modest stabilization alongside Bitcoin. The recent recovery lacks the confirmation necessary to justify aggressive buying. Until our institutional indicators begin aligning, we remain on the sidelines.

🔄 Rotational & Thematic Notes

Improving Sectors

- Semiconductors (SMH)

- Biotech (IBB)

- Equal Weight Biotech (XBI)

Weakening Sectors

- Long Duration Bonds (TLT)

- Precious Metals (GDX)

- Broad Commodity Complex

Institutional Leadership

- Semiconductors (SMH)

- Biotechnology (IBB)

- Equal Weight Biotech

🧠 Tactical Outlook

The market continues working through a healthy consolidation after a strong advance earlier this year. While headline indexes remain resilient, institutional participation remains selective rather than broad-based. We continue emphasizing patience, disciplined risk management, and waiting for high-quality opportunities instead of forcing trades during a mixed environment.

👉 What We’re Watching Now

- Can SPY finally resolve its five-week trading range?

- Will Technology continue carrying the broader market?

- Does TLT resume its larger downtrend?

- Can the U.S. Dollar complete its Backup (BU) and continue higher?

- Will precious metals resume their primary decline?

- Does Bitcoin produce an institutional-quality oversold entry?

- Can SMH, IBB, and XBI continue extending leadership?

🎯 ProTraders CTA

Inside WyckoffSMI ProTraders members receive:

- Institutional Wyckoff analysis

- Relative strength leadership tracking

- Sector rotation dashboards

- Tactical positioning updates

- Wyckoff Alert Engine signals

- Crypto and equity market intelligence

Join WyckoffSMI ProTraders and track institutional money flow in real time.

👉 Join WyckoffSMI ProTraders and trade alongside a professional Wyckoff framework:

WyckoffSMI.com

⚠️ Disclaimer

The WyckoffSMI Week In Review is provided for educational and informational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any security. All commentary reflects a Wyckoff-structure interpretation at the time of publication and may change as market conditions evolve.

Investing involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. WyckoffSMI and affiliated entities may hold positions in securities discussed. Readers are solely responsible for their own investment decisions and should consult a qualified financial professional before acting.

Responses